Farmland Values Rise Again: 2025 Results and 2026 Outlook for the Eastern Corn Belt

By Halderman

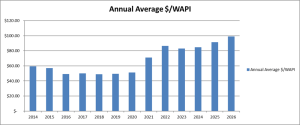

Land Sales Results and Predictions

Commodity prices are near breakeven and volatile; interest rates are near the long-term average and sticky, and input costs remain near historical highs. Fundamentally farmland values should be softer. In many parts of the US this is true, but here in the Eastern Corn Belt farmland remains a strong asset class.

An analysis of the Halderman sales results indicates that land prices shown as dollars per Weighted Average Productivity Point (WAPI) for 2025 finished higher than ever as shown with the blue bars on the chart below. 2025 values are about 8.3% higher than 2024 values.

What is happening in 2026? The chart above shows that on average the cropland we are selling through the first 3 months is up another 8.8% over 2025. One quarter does not make a year, but this year is off to another strong start. That said our sales since the war with Iran broke out are trending a little softer due to the uncertainty around input costs, specifically nitrogen fertilizer and diesel fuel, both of which are up 30% since the war erupted.

Farmland is an excellent hedge against inflation. During the inflationary economic environment of the past 5 years, you can see the rate at which farmland appreciates and once again proves its value as an inflation sensitive asset in your portfolio.

Where do we go from here?

Land values depend on four factors.

- Net farm income

- Interest rates

- Supply of land for sale

- Inflation

A February USDA report estimated that 2026 net farm earnings will be flat versus 2025. If you subtract the federal support payments the net farm income projection would be well below the long term, 20-year average, disaster for those in row crop agriculture. Of course, the federal government stepped in twice so far and maybe a third time later this year with ad hoc support payments to “bridge’ the gap due to reduced trade hurting both our exports of commodities and imports of crop inputs.

Interest rates remain higher than they were just a few years ago. Due to some Fed rate decreases over the past year long term farm mortgage rates are down 90-100 basis points from the recent high. Inflation is sticky and now with the war there are thoughts no further rates cuts will occur. Recession is entering the predictions from economists, so who really knows?

Halderman Real Estate enjoyed a robust 2025-2026 sales season with overall farm transaction numbers up compared to last year. Supply of farms for sale remains below average for the general area. That said we did notice this winter some softer than expected sales in some counties where many acres came to market over the past 12-18 months. If you own land in an area with many recent transactions there might be some weakness, otherwise supply of farms for sale is not burdensome.

Demand remains good for farmland. In the Eastern Corn Belt we benefit from proximity to more people, more economic activity and development. This tends to generate 1031 exchange dollars chasing farmland coming from residential developments, data centers, etc. I think this helps support farmland values in IN, OH and MI more than you find in other Corn Belt states further west.

In summary, land values are steady to slightly higher so far this year when compared to 2025. Demand is good for better than average farms in competitive areas. Demand for lessor quality farms or farms with blemishes is less than it was a year ago. We look for land to remain a strong asset to own with steady prices in 2026. To keep abreast of land values in your area, visit Halderman.com or contact your local representative.